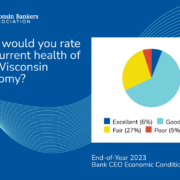

Numbers released today by the Federal Deposit Insurance Corporation (FDIC) showed Wisconsin banks remained in a healthy position through the final quarter of 2023. Banks continued to meet the borrowing needs of their customers, as evidenced by year-over-year lending increases in all categories (commercial, residential, and farm loans). Deposits were up both quarter over quarter (1.12%) and year over year (2.00%), demonstrating public trust in Wisconsin banks as safe places to keep money. While net interest margin has decreased slightly from 3.27% to 3.20% year over year, capital levels are healthy.

Notable indicators include:

Statement on the release of fourth-quarter 2023 Federal Deposit Insurance Corporation (FDIC) numbers from Rose Oswald Poels, president and CEO of the Wisconsin Bankers Association:

“The year 2023 ended on a positive note with banks in a solid position. Residential loans are picking up, while many business owners are tending more toward a ‘wait-and-see’ approach on borrowing. Bankers, consumers, and business owners alike are hopeful that the Federal Reserve will lower interest rates in 2024. Inflation, the potential for a recession, and geopolitical issues remain top concerns for the year ahead. Wisconsin banks continuously evaluate economic conditions and stand ready to serve their customers and communities as trusted financial partners.”

FDIC-Reported Wisconsin Numbers (Dollar Figures in Thousands)

| 12/31/2023 | 9/30/2023 | QoQ Change | 12/31/2022 | YoY Change | |

| Net loans and leases | $109,763,200 | $111,536,925 | -1.59% | $105,370,783 | 4.17% |

| Total deposits | $122,411,348 | $121,056,967 | 1.12% | $120,013,372 | 2.00% |

| Commercial and industrial loans | $17,839,610 | $17,946,778 | -0.60% | $17,804,684 | 0.20% |

| Residential real estate loans | $33,839,052 | $31,436,804 | 7.64% | $32,038,691 | 5.62% |

| Farm loans | $4,031,270 | $5,188,674 | -22.31% | $3,746,971 | 7.59% |

| Total assets | $152,451,299 | $153,646,118 | -0.78% | $149,546,185 | 1.94% |

| Assets 90+ Days Past Due or in Nonaccrual Status | $542,817 | $518,570 | 4.68% | $411,481 | 31.92% |

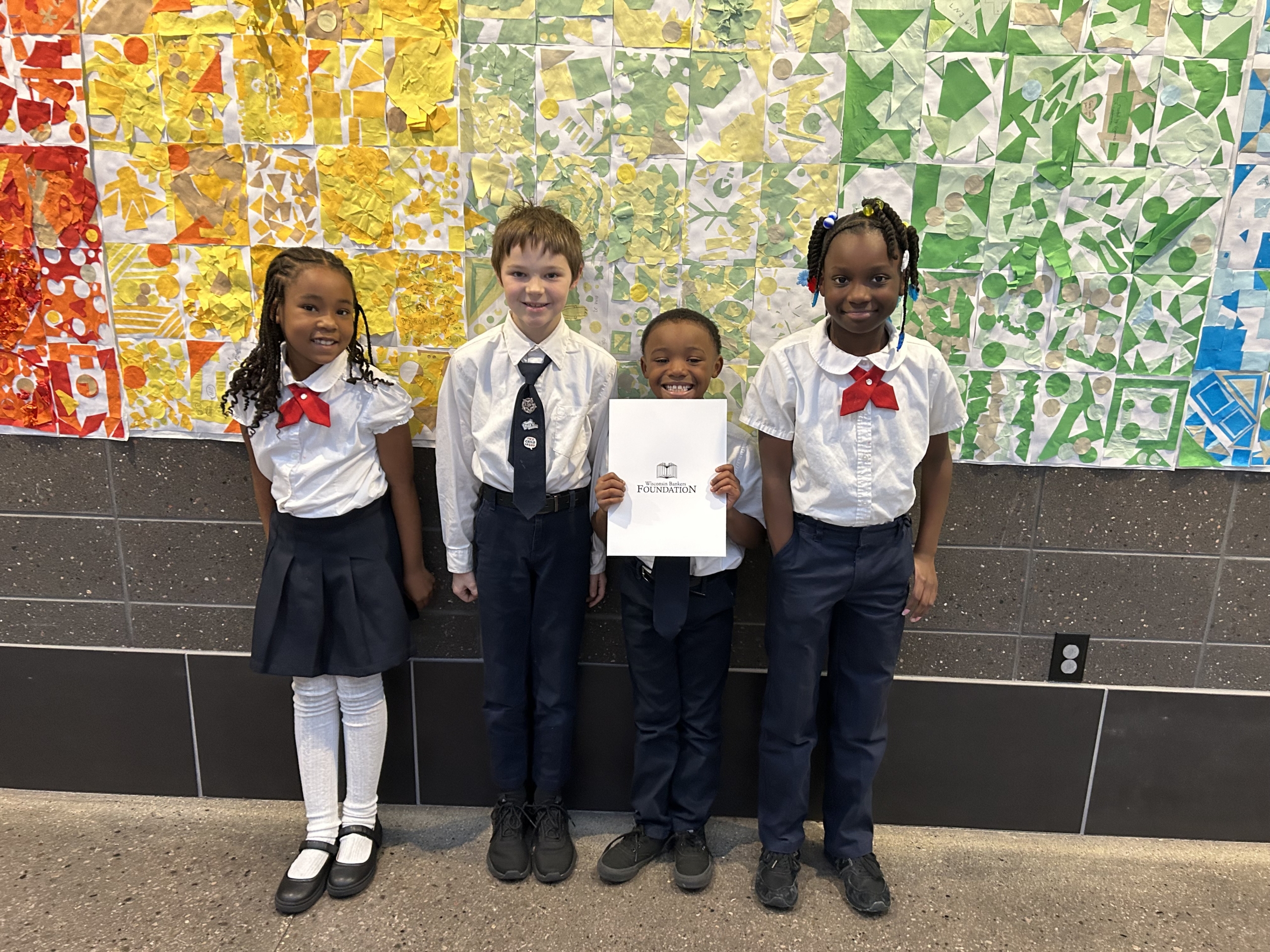

The Wisconsin Bankers Foundation, the non-profit arm of the Wisconsin Bankers Association, has awarded Chad Achenbach and Taylor Lindsay with the 2023 Agricultural Banking Scholarship. Demonstrating the Foundation’s commitment to cultivating the next generation of agricultural bankers in Wisconsin, the Agricultural Banking Scholarship is offered annually in the fall. Two $1,500 scholarships are awarded to students attending an accredited public or private, non-profit college, university, or technical college who demonstrate in their application a strong understanding of the importance of financial literacy and are actively pursuing a career in agricultural finance.

Pictured (left to right) are: Cassandra Krause, executive director, Wisconsin Bankers Foundation; Chad Achenbach, 2023 WBF Agricultural Banking Scholarship recipient; and Cody Kirschbaum, vice president – ag relationship manager, Peoples State Bank.

Chad Achenbach is a declared double major in agribusiness and animal science expected to graduate from UW–Platteville in May 2025. Active throughout the agricultural community, Achenbach grew up on a hobby farm in Eastman, Wis. and was involved with 4-H and FFA through high school. In 2020, Achenbach became an inaugural member of Wisconsin Department of Agriculture, Trade and Consumer Protection’s (DATCP) Wisconsin Agriculture Youth Council, where he gained insight on state agricultural policy development and tools available to support Wisconsin farmers. At UW–Platteville, Achenbach is involved in Alpha Gamma Rho (Beta Gamma chapter), Block & Bridle, and the Pioneer Dairy Club. He also serves as an ambassador for the UW–Platteville School of Agriculture. During the summer of 2023, Achenbach interned at Peoples State Bank in Prairie du Chien, Wis. as an ag loan officer.

Pictured (left to right) are: Michael DeLong, vice president – commercial/agriculture loan officer, Pillar Bank; Cassandra Krause, executive director, Wisconsin Bankers Foundation; Jenny Jereczek, director of agriculture banking & market president – Durand, Security Financial Bank; Taylor Lindsay, 2023 WBF Agricultural Banking Scholarship recipient; Dr. Brenda Boetel, professor and Agricultural Economics department chair, University of Wisconsin – River Falls; and Tony Betley, vice president – senior agricultural banking officer, Nicolet National Bank.

Taylor Lindsay is a declared agricultural business major and animal science minor expected to graduate from UW–River Falls in May 2025. Growing up on her family’s beef farm in Boyd, Wis., Lindsay has been around agriculture her entire life. Involved in 4-H and FFA throughout high school, Lindsay is pursuing an agribusiness career to not only remain active in the agricultural industry but also to help make a difference in her community. At UW–River Falls, Lindsay is a member of the Agricultural Business and Marketing Society, Agribusiness Leadership Team, Block and Bridle, Collegiate Farm Bureau, and Collegiate Livestock Judging Team. During the summer of 2023, Lindsay interned as an agriculture credit analyst at Nicolet National Bank in Eau Claire, Wis.

“In awarding the Agricultural Banking Scholarship to two deserving individuals, the Foundation aims to support and encourage the growth of talent in the agricultural finance sector,” said Foundation Chair Rose Oswald Poels. “I am pleased to recognize Chad and Taylor for their achievements and outstanding commitment to Wisconsin’s agricultural industry and wish them the very best in their future agribusiness careers.”

To learn more about the Wisconsin Bankers Foundation and its current scholarship opportunities, please visit wisbankfoundation.org.

Wisconsin Bankers Foundation Recognizes Outstanding Financial Education Initiative

Rose Oswald Poels (left) and Jaclyn Rutkowski (right)

The Wisconsin Bankers Foundation (WBF) is pleased to announce that National Exchange Bank & Trust, headquartered in Fond du Lac, Wis., has been selected as the recipient of the 2023 Financial Education Innovation Award. The award was presented to National Exchange Bank & Trust representative Jaclyn Rutkowski during a special luncheon on February 8, 2024, in Wisconsin Dells at the largest banking industry event in the state, the Wisconsin Bankers Association (WBA) Bank Executives Conference.

“Too often, people are reluctant to talk or ask questions about finances,” said Rose Oswald Poels, WBF chair and WBA president and CEO. “Through their ‘It’s OK not to know’ campaign, National Exchange Bank & Trust has shared useful financial resources in a fun, accessible way.”

National Exchange Bank & Trust representatives (left to right) Karri Oelke, Jaclyn Rutkowski, and Nicole Wiese

National Exchange Bank & Trust’s multi-media financial education campaign, titled “It’s OK not to know,” ran across digital and social media channels, including TikTok, Facebook, and Instagram. The campaign was designed to engage community members who may not yet feel confident in their financial literacy. Featured content covered topics such as “pay yourself first,” “zero-based budgeting,” and the difference between an adjustable-rate mortgage (ARM) and a fixed-rate mortgage. The campaign included a diverse range of media, such as short-form videos, images with text, emails, and blog posts. The shareable content also emphasized an overarching theme that banks are judgement-free resources, ready to provide support and guidance.

The WBF Financial Education Innovation Award is a prestigious category of the WBF Excellence in Financial Education Awards. Submissions for the 2023 WBF Excellence in Financial Education Awards encompassed over 700 financial education presentations given by 365 Wisconsin bank employees, reaching approximately 25,500 Wisconsin community members.

Federal Deposit Insurance Corporation (FDIC) data released today showed Wisconsin banks remained in good health through the third quarter of this year. Year-over-year lending increased in all categories (commercial, residential, and farm loans), demonstrating the responsiveness of banks to meet their customers’ needs. Individuals and businesses continue to trust banks as a safe place to keep their money, as evidenced by a slight increase in deposits, both year over year (0.59%) and quarter over quarter (0.95%). Net interest margin has held steady at 3.19% year over year, and capital levels are healthy.

Notable indicators include:

Statement on the release of third-quarter 2023 Federal Deposit Insurance Corporation (FDIC) numbers from Rose Oswald Poels, president and CEO of the Wisconsin Bankers Association:

“The newly released FDIC numbers showed that Wisconsin banks remained on solid footing through the third quarter of 2023. Banks continue to be trusted partners in helping individuals, families, and businesses meet their financial goals. As has been the case for several quarters — inflation, interest rates, and geopolitical issues remain concerns heading into 2024. Banks will continue to position themselves to support their communities through potential economic headwinds.”

FDIC-Reported Wisconsin Numbers (Dollar Figures in Thousands)

| 9/30/2023 | 6/30/2023 | QoQ Change | 9/30/2022 | YoY Change | |

| Net loans and leases | $111,535,045 | $109,975,599 | 1.42% | $103,954,503 | 7.29% |

| Total deposits | $121,056,968 | $119,920,909 | 0.95% | $120,347,373 | 0.59% |

| Commercial and industrial loans | $17,946,778 | $18,240,073 | -1.61% | $17,533,085 | 2.36% |

| Residential loans | $31,432,982 | $27,242,091 | 15.38% | $25,109,047 | 25.19% |

| Farm loans | $5,188,674 | $4,824,718 | 7.54% | $4,704,303 | 10.30% |

| Total assets | $153,648,227 | $152,380,455 | 0.83% | $148,567,421 | 3.42% |

| Assets 90+ Days Past Due or in Nonaccrual Status | $518,570 | $434,070 | 19.47% | $417,336 | 24.26% |

The Wisconsin Bankers Foundation, the non-profit arm of the Wisconsin Bankers Association, is pleased to announce a $5,000 grant to St. Marcus School in Milwaukee. The grant will support the St. Marcus community engagement team’s financial education efforts during the 2023–2024 school year, including:

“The work St. Marcus School’s community engagement team is doing to empower the families of their students aligns wonderfully with our Foundation’s mission to promote financial literacy and capability,” said Rose Oswald Poels, chair and treasurer of the Wisconsin Bankers Foundation. “We are proud to support these initiatives and congratulate the St. Marcus staff and participants on the positive impact they are creating.”

St. Marcus School is one of two recipients of a 2023–2024 Wisconsin Bankers Foundation grant. The Foundation also awarded a $5,000 grant as part of a three-year commitment to Asset Builders to support its statewide Finance and Investment Challenge Bowl for high school students.

Second-quarter 2023 data from the Federal Deposit Insurance Corporation (FDIC) show that Wisconsin banks remain on a solid foundation. Banks continue to be responsive to the needs of their customers, and lending increased in all categories (commercial, residential, and farm loans). Deposits also increased slightly as consumers and businesses remained confident in Wisconsin banks as a safe place to keep their money. Net interest margin remains strong at 3.24%, and capital levels are healthy.

Notable indicators include:

Statement on the release of second-quarter 2023 Federal Deposit Insurance Corporation (FDIC) numbers from Rose Oswald Poels, president and CEO of the Wisconsin Bankers Association:

“In the second quarter of 2023, Wisconsin banks showed continued strength and profitability. Banks continue to meet the borrowing needs of individuals, families, and businesses. Deposits have held steady, and delinquencies remain low. While inflation, interest rates, and geopolitical issues remain concerns for the remainder of 2023, banks are prepared for future risks and are poised to support their communities through possible economic challenges.”

FDIC-Reported Wisconsin Numbers (Dollar Figures in Thousands)

| 6/30/2023 | 3/31/2023 | QoQ Change | 6/30/2022 | YoY Change | |

| Net loans and leases | $109,974,664 | $106,543,106 | 3.22% | $99,946,680 | 10.03% |

| Total deposits | $119,920,910 | $118,136,508 | 1.51% | $118,628,924 | 1.09% |

| Commercial and industrial loans | $18,241,734 | $17,700,465 | 3.06% | $17,147,615 | 6.38% |

| Residential loans | $27,242,091 | $26,381,632 | 3.26% | $23,857,546 | 14.19% |

| Farm loans | $4,824,718 | $3,824,265 | 26.16% | $4,446,588 | 8.50% |

| Total assets | $152,378,582 | $149,715,078 | 1.78% | $145,897,591 | 4.44% |

| Assets 90+ Days Past Due or in Nonaccrual Status | $433,555 | $406,287 | 6.71% | $430,201 | 0.78% |